Financial News Friday – October 3, 2014

‘Bond King’ Bill Gross Quits PIMCO For Janus (Reuters)

Legendary bond fund manager Bill Gross left PIMCO, the investment firm he helped found over 40 years ago, for competitor Janus. Gross’s departure comes after have threatened to resign multiple times due to clashes with PIMCO’s executive committee. Gross began managing the Janus Global Unconstrained Bond Fund this past Monday.

Janus’s shares surged by over 40% following the announcement and are now slightly lower but still up around 33% since the announcement at the end of last week.

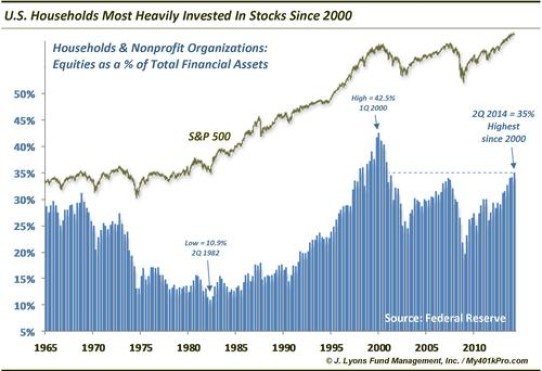

U.S. Households Are The Most Heavily Invested In Stocks Since 2000 (Dana Lyons)

“[In] the 2nd quarter, household and nonprofit’s stock holdings rose from 34.2% to 35% of their total financial assets. This is the highest percentage since 2000. In fact, the blow-off phase from 1998 to 2000 leading up to the dotcom bubble burst was the only time in the history of the data (since 1945) that saw higher stock investment than now.”

Investors typically invest more in stocks as they approach their market tops. Past recessions are long forgotten by that point and many, having been bruised by the most recent recession, are kicking themselves for sitting out of stocks until now. So many pile in and allocate more funds to stocks to make up for the lost gains. Others have seen their portfolios grow due to their allocations in stock and wish to achieve even greater returns by piling more into stocks.

It’s easy to get caught up in the excitement of a bull market, but it’s always important to temper that excitement with a healthy dose of risk management.

The economy doesn’t show any signs of a recession in the near future, but as markets showed us last month, we can expect small (or even larger) pullbacks as the market chugs along. Use this as a reminder for when you wish to allocate more funds to stocks than is necessary for your goals and risk tolerance.

Love Them or Loathe Them, Reverse Mortgages Have a Place (NY Times)

When I was studying financial planning during college, I developed quite a dislike for reverse mortgages. However, after reading several papers on the topic (the one below included) and seeing their possible uses, my mind changed. Reverse mortgages do have a place in some retirees’ financial plans.

You just need to be careful about how you utilize a reverse mortgage.Use it primarily as a risk management tool. Make sure to read the fine print, and utilize a well-known lender with transparent business practices.

The article quotes a paper published in the Journal of Financial Planning by members of the esteemed financial planning faculty of Texas Tech, “many retirees could benefit from paying the closing costs necessary to have a reverse mortgage line of credit (which lenders can’t close down, unlike home equity lines of credit) on standby for times when their investments have fallen. People could then borrow money via the reverse mortgage to live on, and repay it once markets recovered and they could get a better price for selling those investments. The net result is that retirement portfolios can last longer.”

Social Security Cost-of-living Adjustments Projected to Increase Slightly in 2015 (Investment News)

Next year’s cost-of-living-adjustments (COLA) for Social Security beneficiaries are expected to be around 1.7%. From the article, “A 1.7% increase would increase average Social Security benefits by about $20 next year and boost the maximum amount of wages subject to payroll taxes by nearly $2,000 above this year’s $117,000 level.”

Federal Judge Rules Against Obamacare Subsidies (TalkingPointsMemo, TheWeek)

A federal judge in Oklahoma, Judge Ronald A. White, has ruled that Obamacare plans that are sold through federal exchanges are not eligible for tax subsidies; only plans that are sold through the state exchanges are eligible for such subsidies. Judge White states that the ruling was not politically motivated and that he is “upholding the act as written.”

Apparently the verbiage of the massive Affordable Care Act indicates that the subsidies are only available to state-run rather than federally-run exchanges. If upheld, insurance buyers in the 36 states that utilize the federally-run insurance exchange would be ineligible for tax subsidies.

Deadline for Undoing IRA Conversions Approaching Fast (Think Advisor)

If you converted savings from a traditional IRA to a Roth IRA in 2013 and wish to reverse your decision to do so, you should act soon. The deadline for reversing an IRA to Roth IRA conversion (called a recharacterization) is October 15th.

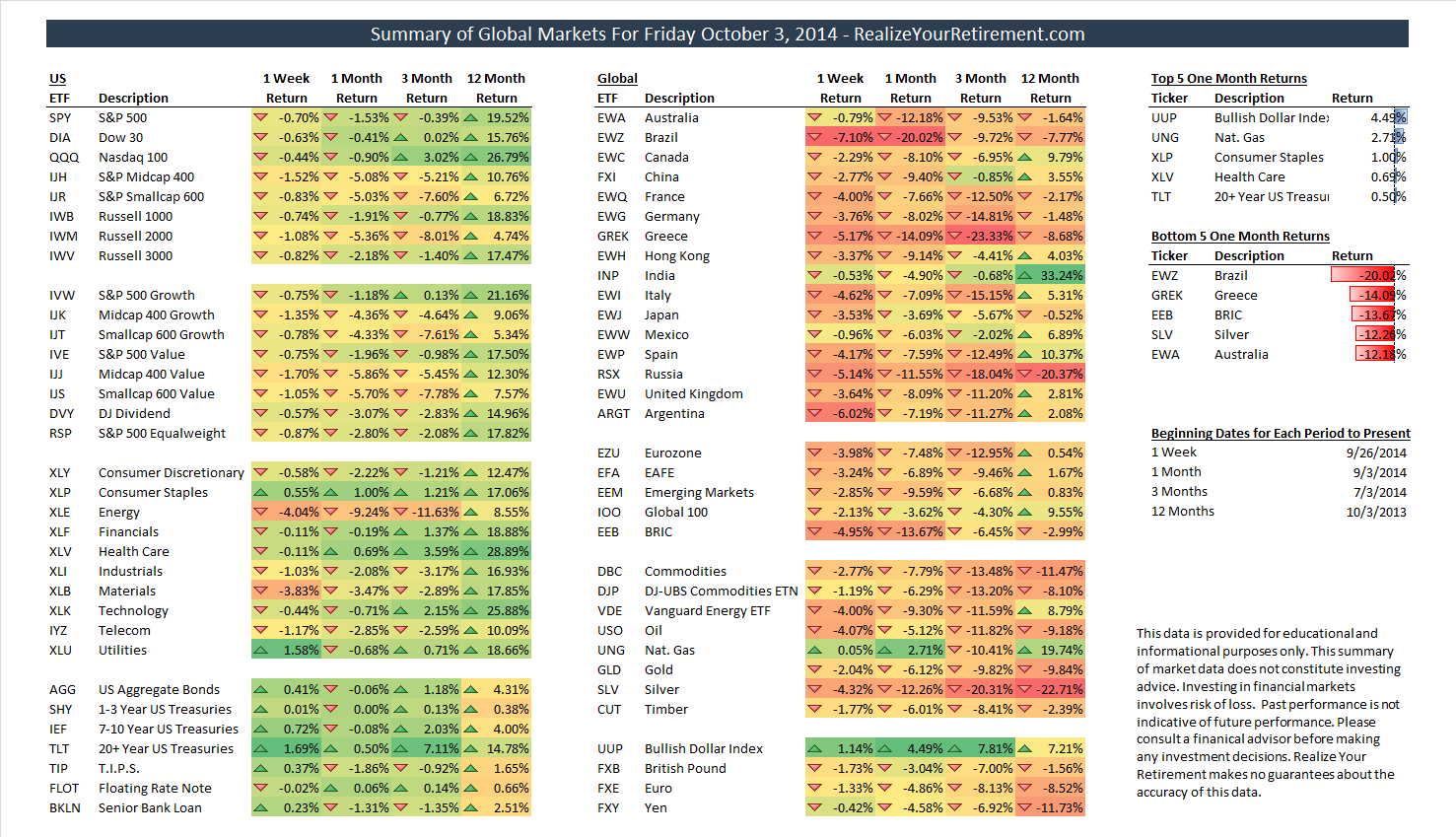

Summary of Global Markets for Friday October 3, 2014

Click the image above to zoom in and see the full Global Market Summary.

Ben ogletree

Have an adviser who is great guy, bu find I’m losing money at a much greater rate than the overall market. This was largely a low risk portfolio?? I’m totally lost as to how to proceed. Retired 7 months ago and invested 1350000. With him in in various instruments including 310000. In variable annuity with jack. Nat. . The port. Gained to 1394000. , but as of today we are back to original investment value???

Dieter

Unfortunately, there are many financial advisors out there who are great people, they just haven’t rigorously researched the products that they sell as financial salespeople. Any relationship will be difficult when both parties aren’t privy to all of the facts, especially when things don’t turn out as the sales pitch portrayed them.

Variable annuities with income riders such as the Jackson National are not meant to control risk for the money you invested into the account. This type of annuity is meant to protect your future income stream, once you begin withdrawals, with a minimum floor, not to protect your current investment dollars. As you may have seen in the review video I posted, this usually amounts to an expected return on the income rider of around 3-4% per year over a 20 to 30 year period, with a breakeven point (when you receive your money back) around 17 years out. If you were to withdraw your money or switch annuities before the withdrawal period (the beginning of the 11th year for most annuities), you would lose the benefits of the future income protection.

The investments offered in the annuity are no different from what you could use outside of the annuity, however, most investments in the annuity have higher fees than their analogues outside of the annuity. So, no matter what diversification or growth you receive within the account, the annuity, income rider, and subaccount fees will cause a drag on your portfolio of up to 2-4% per annum versus a similar portfolio outside of the annuity. Without knowing your exact portfolio, it’s hard to say exactly why your portfolio increased and then decreased, but the drag from fees on a bond heavy (conservative) portfolio could certainly contribute to it.